Agentic AI

The office of the CFO in 2030: how agentic AI changes the equation

Written by

Yogi Goel, CEO

The modern CFO organization is no longer constrained by software. It is constrained by human attention.

For decades, the office of the CFO has invested heavily in financial systems. ERPs, sub-ledgers, billing platforms, payroll engines, and procurement tools have each promised more accurate books and faster closes.

Yet despite these investments, financial operations remain bottlenecked by human capacity.

As companies scale, complexity increases across every dimension. There are more entities, more transaction types, and more fragmented source systems. The volume of accounting work has grown accordingly, but the supply of accounting talent has not kept pace. The CPA candidate pool has declined by 27% over the past decade, and only 1.4% of college students now major in accounting, down from 4% ten years ago.

In practice, this means the modern CFO organization is not limited by its systems, but by the availability of human attention. Teams either expand headcount to keep up, or accept slower close cycles, higher error rates, and increasing operational strain.

This imbalance between growing complexity and limited human capacity has become one of the defining challenges of modern finance.

The cracks are structural

The economics of the CFO organization make this constraint clear. Headcount and consultants account for roughly 90% of finance department spend. This represents a significant portion of the $914 billion spent annually on business operations payroll in the United States. Much of this effort is directed toward repetitive, process-heavy work such as collecting data from fragmented systems, coordinating accrual inputs, matching transactions, and preparing journal entries that are later reviewed and approved.

At the same time, there is increasing evidence that the system is under strain:

These are not isolated failures. They are symptoms of a system that depends on manual effort to maintain accuracy at a scale that no longer matches human capacity.

The function responsible for financial accuracy and performance is spending the majority of its time on work that does not directly drive either outcome.

Where the time actually goes

At its core, the CFO organization serves two primary purposes. It measures and directs financial resources, and it protects the company from financial and regulatory risk.

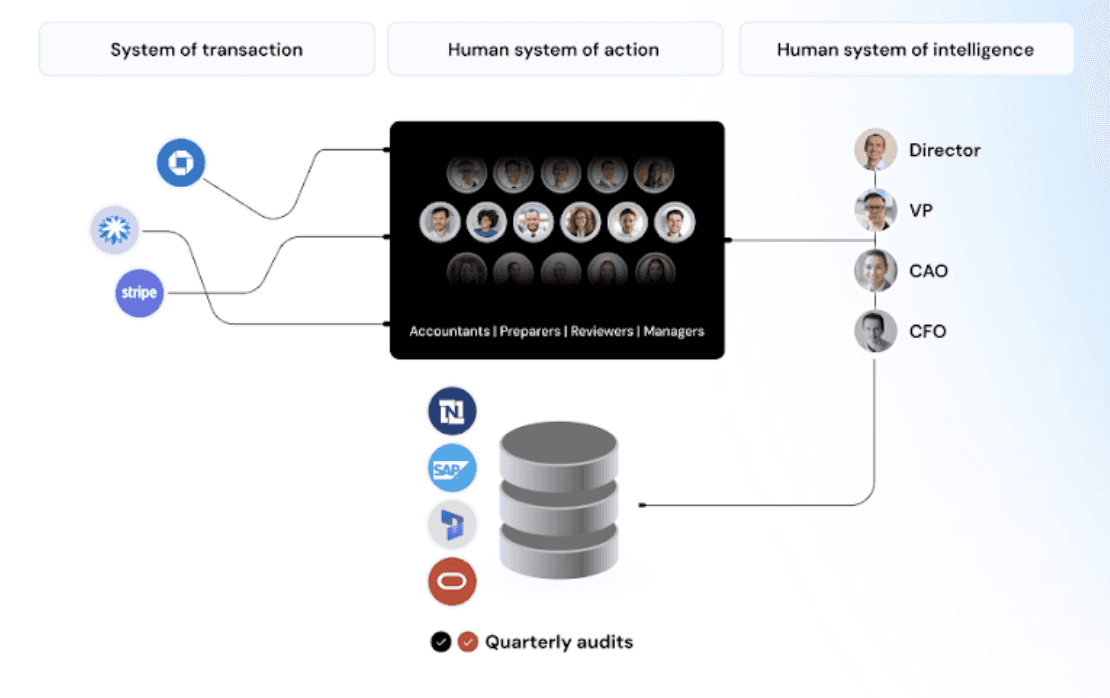

When you strip away org charts and reporting lines, the CFO office runs on three interlocking systems, all connected by manual human effort.

The system of intelligence

This system represents the judgment, domain expertise, and pattern recognition that accounting professionals apply to their work.

At one end of the spectrum is basic logic. For example, identifying when an expense exceeds policy without an approved exception. At the other end is experience-based judgment, such as understanding which variances auditors will scrutinize more closely or recognizing when a flux analysis signals a deeper issue before it is fully apparent in the data.

Between these extremes lies accounting domain knowledge. This includes applying depreciation schedules, interpreting revenue recognition rules under ASC 606, and understanding how different transactions should be treated in context. This layer of intelligence is what ultimately makes financial data reliable.

The system of action

This system encompasses the operational execution of finance processes. It encompasses activities such as sending payment reminders, approving vendor bills, preparing reconciliations, posting journal entries, and generating reports. This layer consumes the majority of CFO organization resources, often around 65% of the budget, and remains largely manual.

The system of transactions and records

This system consists of the platforms where financial data originates and where it is ultimately recorded.

Payroll systems such as ADP, billing platforms such as Stripe, and procurement tools such as Coupa all generate financial data. This data must eventually be consolidated into a system of record, typically an ERP such as NetSuite or Sage. These systems are fundamentally designed to store data. They reflect the inputs they receive, including any errors. They do not inherently understand context, detect anomalies, or identify when a transaction deviates from historical patterns.

Today, these three systems are connected through manual effort. People act as the link between intelligence and execution, between execution and transactions, and between transactions and the general ledger. These connections are inherently fragile. They depend on manual processes and institutional knowledge, both of which introduce risk and variability.

This is the architecture that produced 140 restatements in ten months.

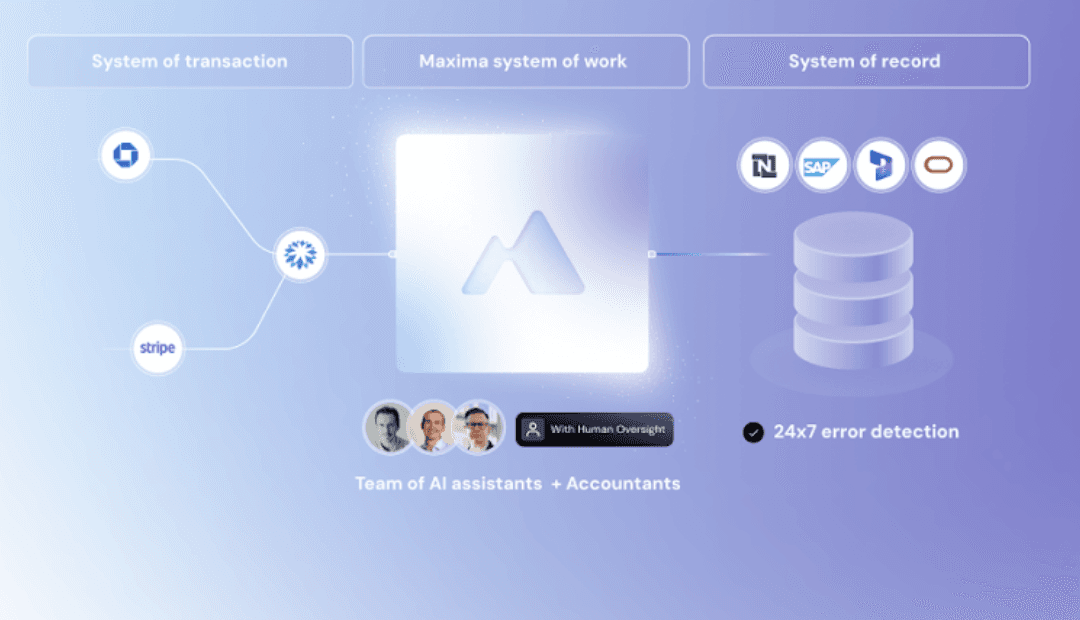

What agentic AI changes about the CFO office

AI as the intelligence layer

Recent advances in AI have introduced systems that can perform many forms of reasoning, pattern recognition, and domain-specific analysis.

In accounting contexts, this enables continuous monitoring of financial data for anomalies, inconsistencies, and policy violations. AI systems are particularly well-suited for detecting patterns across large volumes of transactions, which is where many errors originate.

While certain forms of judgment remain inherently human, AI significantly expands the scope and scale of financial oversight.

Agents as the action layer

The introduction of AI agents represents a more fundamental shift. Traditional automation relies on predefined rules and executes fixed sequences of steps. AI agents can interpret instructions, plan actions, and operate across systems. This changes how work gets done.

A workflow that previously required multiple people across billing, collections, accounting, and reconciliation can now be handled end to end by an agent. For example, an accounts receivable process can move from invoice creation to customer communication, payment tracking, reconciliation, and journal entry creation without human intervention. When a customer underpays, the agent can determine whether it reflects discount terms, timing differences, or an actual exception, and take the appropriate next step.

In effect, agents take on the responsibilities of junior accountants. They prepare work, coordinate across systems, and handle volume at a scale that human teams cannot match. As a result, the structure of the CFO organization evolves. Human teams move away from executing repetitive tasks and toward overseeing, reviewing, and managing exceptions.

Systems of record as infrastructure

As agents take on more operational responsibility, the role of systems of record shifts. ERPs and related systems continue to serve as the foundation for financial data, but they become less central to day-to-day interaction. Instead, they function as infrastructure that supports higher-level workflows.

At the same time, AI-driven monitoring layers operate continuously on top of these systems, identifying risks and inconsistencies in real time.

What agentic AI can do and what stays human

The first step in building a CFO organization for 2030 is accepting a fundamental truth: not all accounting activities should be performed by Agentic AI. The key is understanding which activities can be safely automated, which require human oversight, and which must remain distinctly human.

A three-tier framework

Every accounting workflow can be placed into one of three tiers based on the intersection of error cost, judgment complexity, and regulatory requirements.

Agent-led: full cycle automation with exception handling

These are functions where AI agents can operate independently, with humans intervening only for exceptions or system failures.

Journal entries can be prepared end to end by agents that collect source data, apply accounting rules, calculate amounts, and draft entries based on historical patterns. Controllers review and approve the output. They do not prepare it.

Transaction matching can be performed continuously by agents that reconcile bank activity against sub-ledgers using contextual logic. Instead of flagging every discrepancy, agents can determine when differences reflect expected behavior, such as early payment discounts, rather than true errors.

Account reconciliations and flux analysis can be prepared by agents that compare balances, calculate variances, and identify the drivers of change across periods. Teams review the outputs and focus on the exceptions that require judgment.

Human-in-the-loop: AI does the heavy lifting, humans handle judgment

This middle tier represents where most accounting value will be created. AI handles routine preparation, while humans focus on exceptions, analysis, and strategic decisions.

Revenue recognition illustrates this well. AI can parse contract terms, identify performance obligations, and calculate allocations under ASC 606. Humans evaluate the substance of complex arrangements, including cancellation clauses and variable consideration.

Accrual estimation follows a similar pattern. AI can analyze historical trends and propose estimates. Humans determine whether those estimates reflect current realities.

Intercompany accounting also requires human oversight. Transfer pricing, regulatory considerations, and entity-level requirements involve decisions that extend beyond algorithmic logic.

Human-led: relationships, strategy, and high-stakes decisions

Certain functions remain primarily human due to their reliance on relationships, context, and strategic judgment.

These include audit committee interactions, financial strategy, capital allocation, and regulatory interpretation. These areas depend on experience and organizational context that cannot be fully captured in data.

What this means for finance leaders today

The technologies behind this shift already exist. On standardized benchmarks, AI models have reached roughly the 90th percentile in mathematical reasoning and general reasoning, and have matched or exceeded expert performance in translation, legal reasoning, and coding. The capability curve continues to accelerate.

This transition is already underway:

The companies leading this transition are not waiting for perfect systems. They are deploying agent-prepared workflows today, starting with high-volume, low-judgment processes such as journal entries and transaction matching, and expanding into reconciliations, flux analysis, and close orchestration as confidence builds.

The CFO office of 2030

The CFO office of 2030 will not be a more efficient version of today. It will be a structurally different organization. It will be leaner, faster, more accurate, and more focused on the work that actually determines financial outcomes.

The constraint that has defined finance for decades, human capacity, begins to break. Work no longer scales linearly with headcount. It scales with systems that can operate continuously, consistently, and at volume. The organizations that get this transition right will not just close faster or reduce cost. They will operate with a level of precision, visibility, and control that was not previously possible.

Move closer to an audit-ready, continuous close

Request demo

Insights, news and content

The latest

See all